While recent volatility temporarily stymied the U.S. investment-grade corporate bond primary market, issuers have taken advantage of the newfound calm to resume sales.

Among the deals priced Tuesday, Texas-based disposal company Waste Management (NYSE: WM) sold US$4bn worth of 'BBB'-rated bonds in five parts.

The firm said it intends to use the net proceeds from the issuance to help pay for its US$4.9bn purchase of Advanced Disposal Services (NYSE: ADSW) – announced in mid-April – as well as support its tender offering of up to US$1.3bn and repay commercial paper borrowings.

As of May 9, 2019, Waste Management held roughly US$1.2bn of outstanding borrowings under its commercial paper program, with a weighted average interest rate of 2.70%.

Combining forcesThe merger, which effectively combines the largest and fourth largest municipal solid waste operators in the U.S., primarily aims to expand Waste Management's footprint and customer base.

Under the terms of the agreement, the environmental solutions company stands to gain Advanced Disposal's more than 3 million residential, commercial, and industrial customers, including over 800 municipalities, primarily in 16 states in the Eastern half of the U.S. Its solid waste network includes 94 collection operations, 73 transfer stations, 41 landfills, and 22 owned or operated recycling facilities.

Waste Management underscored its target's US$1.56bn in 2018 revenues, adjusted EBITDA of US$427m, as well as a workforce of around 6,000 employees.

Jim Fish, Waste Management's CEO, said that with this acquisition, "we will grow our asset footprint to serve more customers and communities and generate significant growth and value creation opportunities for Waste Management's shareholders and our combined company's employee base.

"Waste Management's disciplined capital allocation and balance sheet strength position us well to execute upon this unique opportunity to expand our scale and capabilities to serve an even broader customer base and realize the strategic and financial benefits the acquisition of Advanced Disposal creates."

The transaction is expected to close by the first quarter of 2020, and, if successful, Waste Management expects to maintain its investment-grade credit profile, with a pro-forma leverage ratio within its long-term targeted net debt-to-EBITDA range of 2.75x to 3.0x.

Fitch Ratings assigned a 'BBB+' rating to the US$4bn senior unsecured note sale, which was comprised of tenors of five, seven, 10, 20 and 30 years.

Fitch analysts Carlos Benedict and Stephen Brown noted that while the tie-up will "substantially" increase Waste Management's debt burden, it expects the company to use its "strong" free cash flow (NYSE:FCF) to reduce leverage over the 12 months following the acquisition close.

Fitch expects adjusted debt/EBITDAR and FFO adjusted leverage to fall below 3.0x and 3.5x, respectively, within a year of the transaction.

Fitch said that although it expects the company will prioritize debt reduction over the intermediate-term, the "incremental leverage will reduce headroom in the rating, and any further debt-funded acquisition activity or a decision by the company to prioritize share repurchases over de-levering could result in a negative rating action."

The US$4bn note deal was co-lead managed by Credit Suisse, Deutsche Bank Securities, Goldman Sachs, J.P. Morgan and Mizuho Securities.

Demand remains ripeMeanwhile, demand for the issuance was generally fervent, with spread compression of around 12.5 basis points to 20bps across the tranches. Most of bond investors' interest appears to have been focused on the deal's five-year notes, which priced at a spread of 75bps more than matched-maturity U.S. government debt – a narrowing of 20bps from its initial price talk.

Overall, Waste Management's issuance contributed to seven investment-grade corporate bond sales Tuesday, totaling US$10.4bn, according to figures compiled by Ron Quigley, head of fixed income syndicate at Mischler Financial. It fell alongside other iconic industrial names such as Caterpillar Financial (NYSE: CAT), which sold a US$2bn bond in three parts.

Quigley added that the company's sale accounted for nearly 40% of Tuesday's volume "post-positive Trump comments that a trade war deal can still be hammered out between the U.S. and China," which helped ease market tensions.

Indeed, high grade corporate debt continues to attract global demand for the yield offered in the primary market – especially among those bond buyers who have been priced out of their local markets or have a dearth of available paper.

The yields on 10-year Japanese and German government bonds, for example, were last in the areas of -0.065% and -0.100%, respectively.

Fund flows also continue to swell.

For the week ended May 8, Thomson Reuters/Lipper U.S. Fund Flows reported a net inflow of roughly US$3.33bn into investment-grade corporate bond funds, while high yield funds posted net outflows of just US$212m.

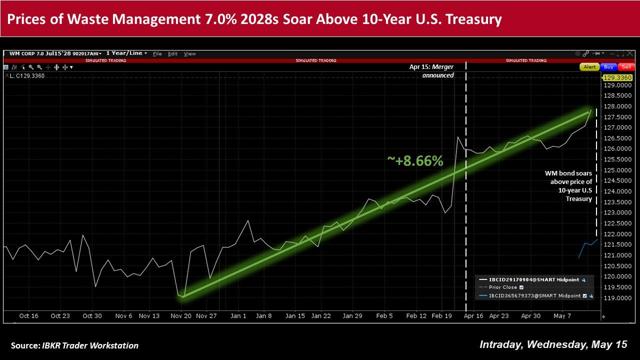

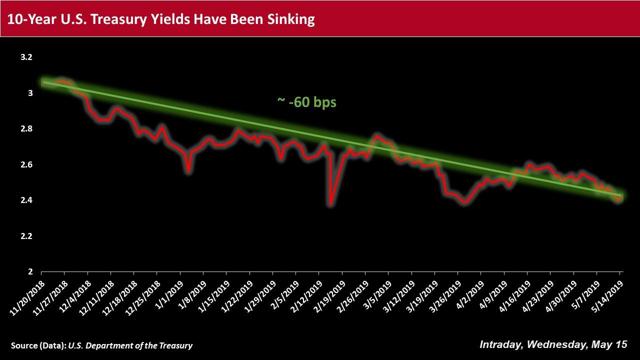

Secondary performance of certain high-grade notes has also been on the upswing, as U.S. Treasury yields have fallen recently.

Prices of Waste Management's 7.0% notes due July 15, 2028, for example, have risen about 8.66% from its 52-week low set in late November 2018 to a new one-year high of US$129.336 intraday Wednesday, according to the IBKR Trader Workstation. Over that period, the yield on the 10-year U.S. Treasury note has fallen by almost 70bps. That note was last trading at around 2.38% intraday Wednesday.

While geopolitical tensions and fears of slowing global growth have generally helped prices of U.S Treasuries to rise, the Federal Reserve's recent decisions to maintain the target range for the federal funds rate at 2.25-2.5%, with no plans in 2019 to hike interest rates further, as well as cease other quantitative tightening measures, have also spurred a plunge in government bond yields, which effectively helped to reignite a decent degree of risk appetite amid lower borrowing costs.

Note: This material was originally published on IBKR Traders' Insight on May 15, 2019.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. Business relationship disclosure: I am receiving compensation from my employer to produce this material.

0 comentários:

Postar um comentário