Summary

Waste Management is a leading provider of comprehensive waste management services.

The company has recently made considerable investments in Sweden and plans for the bottom line acceleration this year.

The valuation suggests the company's shares could offer an outstanding long-run annualized return potential.

Investment ThesisShares of Waste Management Inc. (WM), a leading provider of waste management services in the United States, have recorded a period of stable appreciation, which could be possibly extended as defensive stocks usually perform well regardless of the general economic environment.

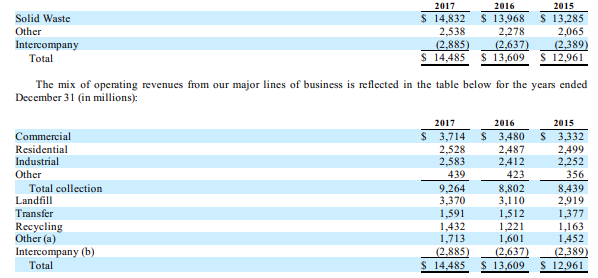

Corporate profileWaste Management is a waste management service company operating across the United States. Besides traditional disposal and recycling services, it offers personal counseling services regarding specialized waste such as bulbs, batteries, electronics and medical equipment as well. According to the company CEO's message, in the past, Waste Management was exporting about a third of residential recyclables to China. Last year, however, China began implementing new recycling and environmental policies, which changed this business practice. Currently, the company has over 42,000 full-time employees and operates three revenue segments, of which two are profitable. Apart from that, its revenue can be divided into nine major business lines, which are captured in the table below:

Source: Waste Management's 2017 10-K

Key takeaways from the latest earnings callAs indicated during the latest quarterly earnings call, company management's plan for the next few quarters is to accelerate the growth of the bottom line. Waste Management has made significant investments in Sweden, which are expected to drive strong organic growth over the next few years. In the last quarter, the company executed well on its strategy and plans to pass on the higher contamination costs to its customers through price increases in late Q4 last year.

''We are seeing very strong organic growth in our highest return businesses, and we expect that to continue. So we are making valuable investments in our Sweden (21:22) landfills that position us well to continue to respond to growth.''

- Devina A. Rankin, Senior Vice President and Chief Financial Officer

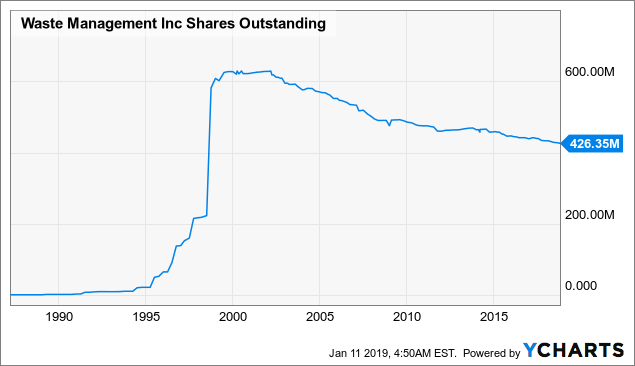

Decreasing the number of shares outstandingA big positive on Waste Management's corporate policy is the fact that since the millennium, the number of shares outstanding has been gradually decreasing at a steady rate of around 2 percent annually. In December 2015, the company authorized a share repurchase program of 1 billion U.S. dollars, and in each of the following years, repurchased its common stock worth $600+ million.

Source: Waste Management's 2017 10-K

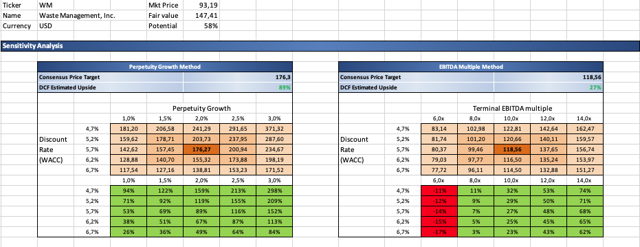

ValuationPlugging in Waste Management's financial statements' figures into my DCF template, the company's shares seem to be fairly undervalued. Under the perpetuity growth method with a terminal growth rate of 2 percent, constant 5 percent annual revenue growth over the next five years and 18 percent EBIT margin, the fair value of the stock comes at US$176. Under the EBITDA multiple approach of a discounted cash flow model, the intrinsic per share value of the company stands roughly at US$118.6, if we assume that the appropriate exit EV/EBITDA multiple in five years' time is around 10x.

Source: Author's own Excel model

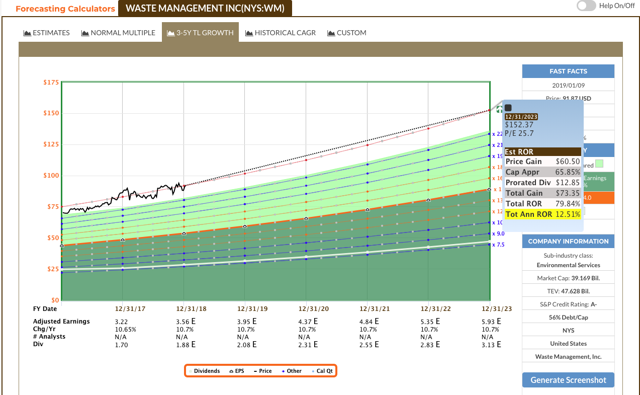

From a different perspective working with operating earnings multiples, Waste Management's shares seem to be currently more or less fairly valued, accounting for the dividends. Using the F.A.S.T. Graphs forecasting calculator with a default 10 percent adjusted operating earnings growth rate assumption, the company's intrinsic value is forecasted to reach US$133 by the end of December FY2023, which implies a total annualized rate of return upside potential of approximately 10 percent.

Source: F.A.S.T. Graphs

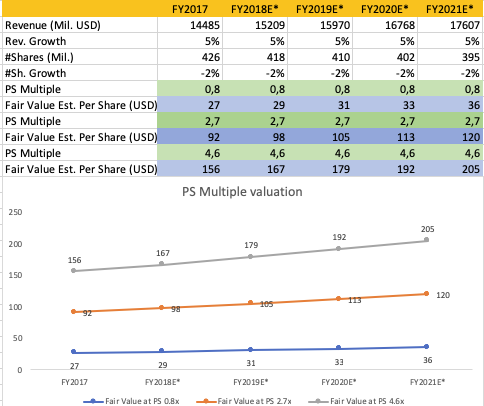

Lastly, in the light of revenue variation of Peter Lynch's popular earnings line for the projection of intrinsic per share values of the company, Waste Management's shares appear to provide the greatest room for appreciation. According to my model, assuming 5 percent annual revenue growth, a two percent annual equity dilution factor, and a price-to-sales ratio of around 2.7x, the company's share price could reach US$120 by the end of 2021. This scenario suggests an average potential annualized rate of return of approximately 8 percent in the following years. Should the company's price-to-sales ratio continue in its expansion channel, the shares could offer up to 30 percent annualized return potential with respect to their current market price.

Source: Author's own Excel model

Key risksTo sum up, Waste Management is an intriguing business with a lot of business resilience, which can prove to be an important characteristic, especially in a volatile economic environment. The company has a solid balance sheet and income statement, with bottom line expansion initiatives in progress.

Disclaimer: Please note that this article has an informative purpose, expresses its author's opinion, and does not constitute investment recommendation or advice. The author does not know individual investor's circumstances, portfolio constraints, etc. Readers are expected to do their own analysis prior to making any investment decisions.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

0 comentários:

Postar um comentário